The Synchronization Layer: Why Tokenization Fails Without Institutional Data Rails

June 2026

Bering Waters Ventures is a strategic investment and advisory firm focused on supporting the next generation of blockchain innovators. Specializing in early-stage investments, we provide not only capital but also hands-on advisory, facilitate strategic partnerships, and help projects build relationships with investors—to ensure their success and scalability.

Our commitment extends beyond investment — we actively collaborate with our portfolio companies and broader market participants to drive sustainable growth and long-term impact, while contributing to the overall advancement of the blockchain industry in an evolving and competitive landscape.

Through this report, Bering Waters Ventures aims to contribute to the evolving discussion around real-world asset tokenization, highlighting why tokenization alone is insufficient without the continuous synchronization of off-chain data. By exploring the infrastructure required to keep tokenized assets aligned with their underlying economic reality, this report examines the emergence of a new institutional data layer that may prove as critical as tokenization itself.

Executive Summary

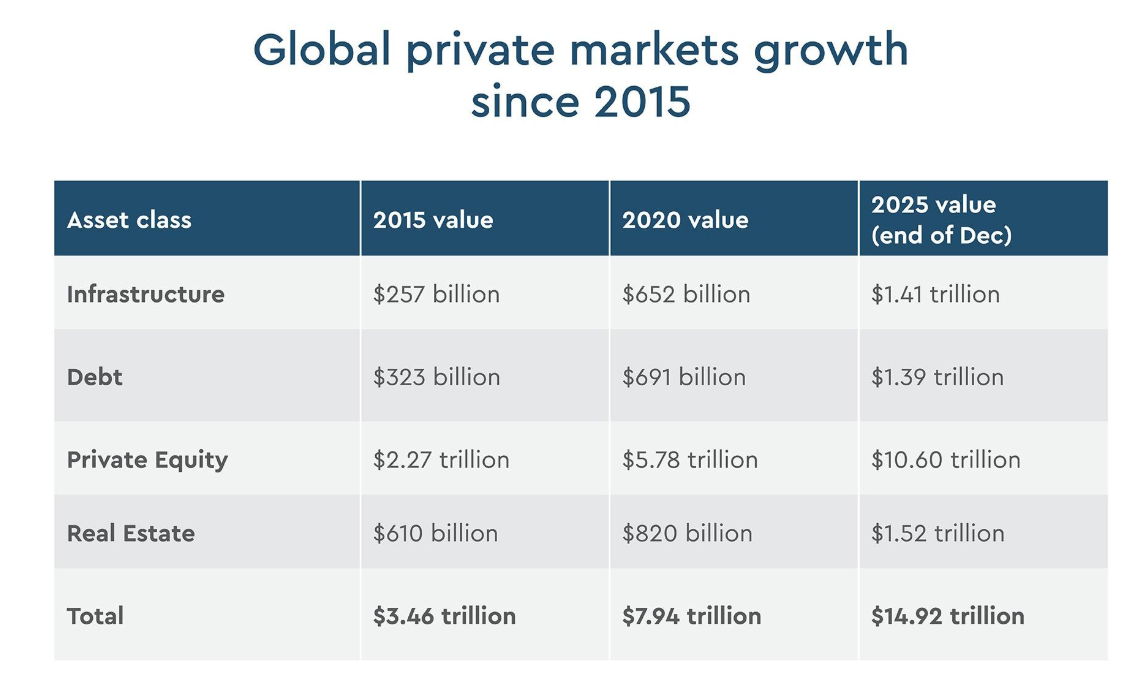

Capital markets are undergoing a quiet structural shift. A multi-year decline in public listings and traditional capital raising has pushed global asset managers to hunt for yield in private markets: private credit, commercial property debt, residential mortgage portfolios, and infrastructure. Global private capital held in funds reached a record $14.9 trillion at the end of 2025, up 15.4% in a single year.1 The migration is real, it is large, and it is accelerating.

But there is an infrastructure chasm standing in its way. Public markets run on continuous, real-time information. Private markets do not. They were built around periodic reporting, bilateral relationships, and manual administration. A UK Financial Conduct Authority review found that private market assets are still typically valued only quarterly — and, for some private debt, monthly at best.2 An asset that re-prices every ninety days does not belong, unmodified, on a ledger that settles every few seconds.

This is the reality the tokenization conversation keeps missing: tokenization alone does not solve the private-market infrastructure problem. Wrapping an opaque, quarterly-valued private credit fund in a token does not make it liquid. It simply places a stale, illiquid asset onto a 24/7 rail. The token is the easy part. Keeping that token continuously synchronized with the asset's real-world value, ownership, compliance status, and servicing events is the hard part, and the part that actually creates a market.

The evidence is already on-chain. BlackRock's tokenized Treasury fund, BUIDL, did not become significant because Treasury shares were represented as tokens. It became significant when those tokens could be used as collateral across trading venues, and by early 2026, traded directly through decentralized liquidity. None of that works without a live data layer publishing the fund's value and proving its reserves, continuously, everywhere the token travels. Apollo's tokenized private credit fund, ACRED, did not gain utility from digitization; it gained utility when verified fund data could be delivered into on-chain lending markets, letting the asset be borrowed against and put to work. In both cases, the enabling factor was not the token. It was the data plumbing underneath it.

This is what we call the synchronization layer - the infrastructure that keeps a tokenized asset aligned, in real time, with the systems that determine its value. It is the unglamorous plumbing that turns a static digital wrapper into a functional financial instrument. And it is becoming the real competitive battleground in institutional finance: not only those who can issue a token, but also those who can keep it synchronized.

This paper makes three arguments about why that layer is hard, and why it is decisive:

• The economics of data delivery have to change: The crypto-native habit of constantly "pushing" prices on-chain is wasteful for institutional assets that do not move every second. A modular, "pull-based" model keeping signed data off-chain until the moment of execution is dramatically cheaper and is the only economically rational design at institutional scale.

• Privacy is the precondition for private markets: Institutions will not broadcast loan performance, yield mechanics, or client whitelists onto a public ledger. The synchronization layer must verify sensitive data off-chain and pass only a cryptographic proof on-chain — confidentiality preserved, integrity intact.

• Fragmentation is the silent killer: Assets are being tokenized across private bank chains, Ethereum layer-2s, and alternative layer-1s. An asset tokenized where its buyers are not is operationally stranded. Real synchronization means aligning an asset's value and compliance rules across many ledgers at once.

Tokenization without institutional data rails is a theoretical exercise. The institutions that win the next decade will be the ones that keep the issued tokens continuously connected to the real economy.

Chapter 1. From Price Feeds to Plumbing

The first generation of blockchain data infrastructure answered one question: what is the current price of an asset? In the closed world of decentralized finance between 2018 and 2020, that was enough. Lending protocols needed to value collateral and trigger liquidations; "oracles" bridged exchange prices on-chain, and the model worked well for what it was.

Because the question has changed. As real-world assets move on-chain, the industry no longer needs only prices. It needs net asset values, interest rates, corporate actions, proof of reserves, servicing events, ownership records, and compliance triggers delivered continuously and reconciled against systems that live entirely off-chain. The role is no longer data delivery. It is orchestration: coordinating valuations, settlement instructions, eligibility checks, and asset-servicing events across blockchains and the traditional institutions that still hold the legal record.

That is the graduation from a crypto sandbox to Wall Street rails, from telling a smart contract what a token costs, to keeping a tokenized fund aligned with the administrator, custodian, transfer agent, and regulator that govern it. The technology that does this deserves a more accurate name than "oracle." It is a synchronization layer - and the rest of this paper is about why that distinction is not semantic but structural.

Chapter 2. The Capital Migration and the Infrastructure Chasm

To understand why this matters now, let’s follow the money. Public markets have been contracting as a venue for capital formation - fewer IPOs, fewer public raises, companies staying private longer. Forced to find yield and differentiated return elsewhere, pension funds, insurers, sovereign wealth funds, and asset managers have moved decisively into alternatives. Private credit in particular has become one of the fastest-growing segments in global finance. The result is the $14.9 trillion private-capital pool, and a structural dependence on asset classes that were never built for continuous markets.3

This is where the chasm opens. Public securities come with real-time prices, standardized disclosure, and observable transactions. Private assets come with none of that. Valuations are periodic and model-driven; the FCA's review of private-market valuation practices found quarterly cycles to be the norm, with the regulator explicitly flagging the risk of stale valuations when investor reporting runs more frequently than the underlying valuation process. Price discovery is thin because many private loans are originated to be held, not traded. Administration is spread across custodians, fund administrators, transfer agents, valuation agents, and servicers, each maintaining its own records that must be reconciled after the fact. Settlement still leans on message-based coordination between separate systems.

These inefficiencies were tolerable when private assets were illiquid by design and held for years. Tokenization breaks that tolerance. The moment ownership becomes digitally transferable, market participants begin to expect the transparency and responsiveness they have everywhere else — and the gap between a 24/7 rail and a 90-day valuation becomes not a technical inconvenience but a structural fault line. Closing it is not a nice-to-have feature. It is a legal and economic necessity because an asset cannot be safely collateralized, margined, or settled against a number that is three months old.

Chapter 3. Not All Assets Are Equal: The Synchronization Profile

Before going further, it is worth dispelling a common simplification. Tokenization discussions tend to treat "real-world assets" as a single category, implying that one infrastructure stack can serve them all. The opposite is true. Each asset class generates a different synchronization profile - a different mix of update frequency, data complexity, and compliance burden - and the failure mode of most tokenization projects is designing for the token rather than for that profile.

| Asset class | What must stay synchronized | Frequency | Hardest requirement |

|---|---|---|---|

| Treasury & money-market funds | NAV, collateral value, and eligibility | Daily to real-time | Speed and cross-venue consistency |

| Private credit & loans | Loan performance, covenants, cash flows, and NAV | Periodic, but event-sensitive | Confidentiality |

| Real estate & alternatives | Title, appraisals, servicing, distributions | Event-driven | Legal reconciliation (on-chain vs. registry) |

| Public equities & ETFs | Price, corporate actions, shareholder records | Real-time | Error tolerance near zero |

| Commodities & natural resources | Reserves, production, attestation | Event-driven | Proof of physical existence |

A tokenized Treasury fund needs speed; a private credit vehicle needs confidentiality; real estate needs legal reconciliation; commodities need proof that the asset physically exists. These are not variations on one problem; they are different problems wearing the same digital wrapper. The institutions that succeed will be those that understand the underlying asset's data environment and build synchronization accordingly. The three structural realities that follow are the properties that determine whether an infrastructure can serve the harder end of this spectrum at all.

Chapter 4. Three Structural Realities

Solving the institutional chasm isn't just a matter of moving data; it requires rethinking the fundamentals of how that data is delivered. The previous chapters established the problem: a wave of capital migrating into private assets that were never built for continuous markets, and a tokenization narrative that mistakes issuing a token for solving that gap.

Closing this gap means more than pointing an existing oracle at a new asset. The assets driving this shift are slower-moving, more sensitive, and more scattered across competing ledgers than anything crypto-native infrastructure was designed for, and each of those characteristics breaks one of the assumptions on which first-generation data delivery was built on.

Three properties, in particular:

Separate infrastructure that can genuinely serve institutions from infrastructure that merely delivers prices - the economics of how data is published,

The privacy with which it is handled, and

The consistency with which it is maintained across chains.

Each is a place where the crypto-native default is not just suboptimal for Wall Street but actively wrong.

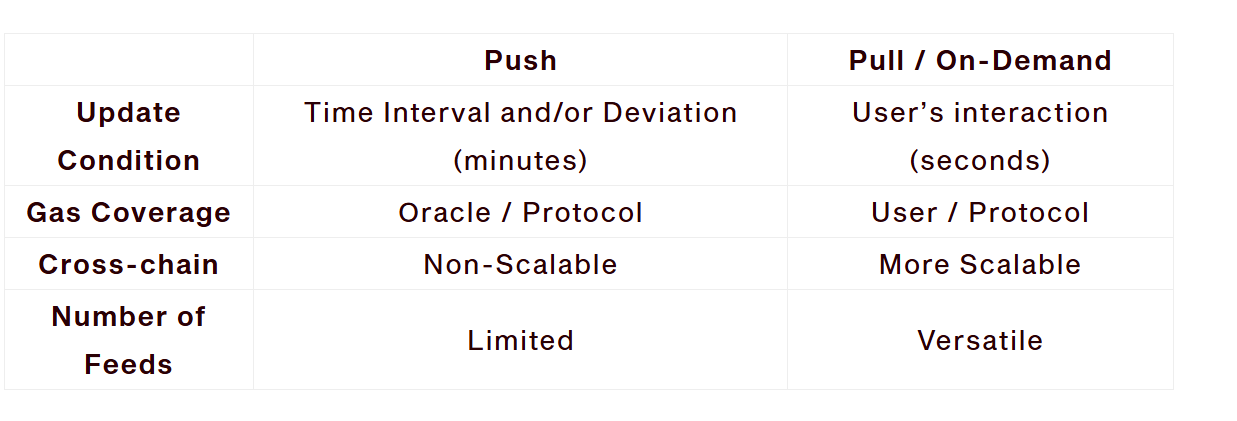

4.1 The Economics of Push vs. Pull

Most first-generation oracle systems are "push"- based: data providers continuously write updates on-chain at fixed intervals or whenever a price crosses a threshold. For assets that trade every second with crypto-like volatility, that constant publishing is defensible. For institutional assets, it is a structural waste.

A tokenized Treasury fund's NAV does not lurch second to second. A private credit valuation may change quarterly. Paying to write that data to a blockchain thousands of times a day, consuming block space and transaction fees regardless of whether any application needs the update, is a recurring tax on assets that do not move. Multiply it across thousands of feeds and multiple chains, and the "push" model becomes a meaningful, permanent cost center that scales the wrong way: the more an institution tokenizes, the more it pays to keep dormant data alive.

The alternative is a modular, "pull" based design. Data is sourced, validated, and cryptographically signed off-chain, then brought on-chain only at the exact moment a transaction requires it - at execution. The integrity guarantee is identical (the signature proves authenticity), but the asset is no longer paying to broadcast a number nobody is reading. For institutional balance sheets, this is the difference between infrastructure that is economically rational at scale and infrastructure that is not. It also has a second-order benefit that matters more in private markets than in crypto: data that stays off-chain until execution is not sitting exposed on a public ledger between updates. The market is converging on pull-based and hybrid architectures for real-world assets, reserving continuous push for the genuinely high-frequency cases where it earns its cost.

4.2 The Privacy Imperative

The second reality is the one institutions raise first, and the industry addresses last. A private credit manager will not publish loan-level performance, covenant status, yield mechanics, or its investor whitelist onto a public ledger for competitors and counterparties to read. Confidentiality is not a preference in private markets; it is the product. Any synchronization model that requires sensitive data to be posted in the clear is dead on arrival for exactly the asset classes driving the capital migration.

This is why the more important capability is not publishing data but proving it. Next-generation data layers can ingest sensitive information off-chain, verify it, and pass only a cryptographic attestation (a proof) to the smart contract. The chain learns that a covenant is met, a reserve is fully backed, or an investor is eligible, without ever seeing the underlying numbers. Three mechanisms make this practical:

Permissioned metadata, where sensitive fields are held in controlled environments and only authorized parties can resolve them

Verifiable attestations, where a trusted validator signs a statement about the data, and

Zero-knowledge-style proofs, which demonstrate mathematically that a fact holds - a value sits within a range, a rule is satisfied - while revealing nothing else.

Proof-of-reserve and proof-of-asset frameworks are the early, visible examples; the broader principle, verify off-chain, attest on-chain, is what makes private alternatives tokenizable at all. For a public-markets asset, transparency is a feature. For a private-markets asset, the ability to coordinate that a fact is true without disclosing what the fact is becomes the whole game.

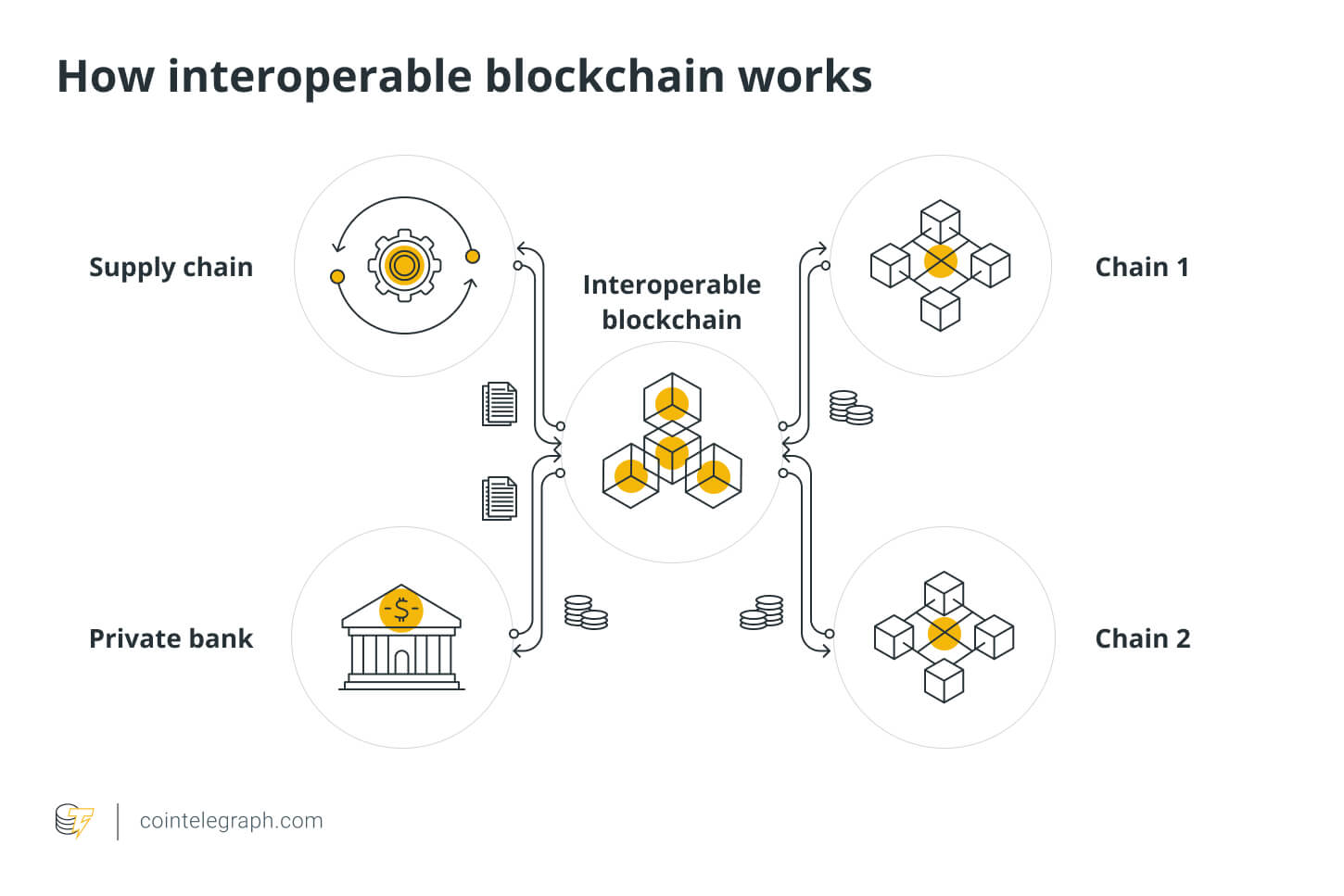

4.3 The Multi-Chain Trap

The third reality is fragmentation. Tokenization is not happening in one place. It is happening on private bank chains, on Ethereum layer-2s, on alternative layer-1s, and on permissioned enterprise networks, simultaneously and without coordination. That creates a trap. If an asset manager tokenizes a property-debt portfolio on one network while its institutional buyers and their collateral sit on a different banking rail, the asset is operationally stranded. Liquidity that cannot reach the asset is not liquidity.

The basic fix, pick one chain and force everyone onto it, will not happen because the largest institutions are deliberately building on their own rails. The real solution is cross-chain state synchronization: keeping an asset's NAV, its compliance permissions, and its ownership record aligned across many ledger environments at the same time, so the token represents the same thing everywhere it exists. This is closer to how correspondent banking and market-data distribution already work than to anything crypto-native; it treats blockchains as a set of venues to be kept in agreement, not a single platform to be standardized onto.

Notably, this is the same conclusion central banks have reached. The Bank for International Settlements' Unified Ledger concept and the Bank of England's Project Meridian both argue that synchronization between systems matters more than forcing all participants onto one.4 When an asset can move to where its liquidity is without losing its identity, fragmentation stops being a tax and starts being a feature.

Chapter 5. Proof in Production

The synchronization layer is already load-bearing in live institutional deployments, and the most instructive cases show, precisely, that the token was never the point.

BlackRock and Securitize - BUIDL.

Launched in March 2024, BUIDL became the largest tokenized Treasury fund in the market.5 But its significance came after issuance. Tokenized fund shares are operationally inert until they can be used, and BUIDL's utility compounded as it was accepted as collateral - first through prime brokers, then across trading venues including Crypto.com and Deribit in mid-2025, and Binance later that year.

Then, in February 2026, BlackRock and Securitize went a step further, enabling BUIDL to trade directly through decentralized liquidity via UniswapX, with BlackRock making a strategic investment in the protocol.6

Each of those steps required the same thing: every venue relying on a consistent, continuously published representation of the fund's value and reserves. A fund share is only collateral if everyone can trust what it is worth at the moment they accept it. That trust is a data problem, and solving it is what turned BUIDL from a tokenized fund into a financial primitive.

Apollo, Securitize, and Morpho - ACRED.

If BUIDL shows tokenized cash, ACRED shows tokenized private credit — the harder, more valuable case. Apollo's diversified credit exposure, tokenized via Securitize, became genuinely useful when it could be put to work in on-chain lending: holders could access a leveraged strategy routed through Morpho's lending markets, with risk parameters managed by a specialized curator.

That only functions if the lending market can continuously verify what the fund is worth and what backs it. The oracle delivering that NAV and powering the integration is RedStone; the asset's holdings are independently attested on-chain through proof-of-asset verification.7 The lesson is exact: digitizing the fund was not the key element; synchronizing verified fund data into a lending venue created the credit market.

ACRED is the Privacy Imperative of Section 4.2 made concrete. A private credit fund cannot broadcast its loan-level performance or borrower exposures onto a public chain; that confidentiality is the product. The position works precisely because the sensitive underlying data is verified off-chain and only what the market actually needs reaches the ledger: a trusted valuation, and a proof that the assets exist. RedStone's model of sourcing and verifying off-chain and delivering signed data on-chain lets the lending market price, margin, and lend against the fund without the fund ever exposing its book. This is the bridge from theory to production - the abstract argument that private alternatives require "verify off-chain, attest on-chain" turns out to be the exact mechanism that lets an opaque, quarterly-valued credit fund become live, borrowable collateral.

DTCC - the Collateral AppChain.

The clearest institutional validation comes from the center of the system. The Depository Trust & Clearing Corporation, which sits beneath much of global post-trade activity, is building a tokenized Collateral AppChain to enable near-real-time, 24/7 collateral mobility — continuous valuation, margining, and settlement in place of end-of-day batch reconciliation.

Announced in May 2026 with a production target later in the year, it runs on the Chainlink Runtime Environment and a shared data standard.8 The point is not the blockchain. It is that effective collateral management requires a constant flow of agreed-upon information between trading systems, valuation engines, custody platforms, and settlement infrastructure. DTCC's bet is that the future of market plumbing is synchronization between institutions, not consolidation onto one platform.

The same pattern repeats across a widening field, and each case is worth seeing for what it synchronizes rather than what it tokenizes:

• J.P. Morgan (Kinexys) and Ondo. Kinexys settled its bank deposit token against Ondo's tokenized Treasuries in a cross-chain delivery-versus-payment test, with the payment leg and the asset leg living on different chains and an interoperability layer coordinating an atomic exchange.9 The asset moves only when the cash moves, which requires both ledgers to agree on the state at the instant of settlement.

• State Street and Galaxy. Their tokenized liquidity fund (SWEEP) brings institutional cash management on-chain, publishing a daily NAV on-chain and supporting cross-chain interoperability while traditional custody and transfer-agency functions remain intact.10 It is a tokenized fund, not a stablecoin; the distinction matters because the value comes from synchronizing fund administration with programmable rails.

• SWIFT and UBS Asset Management. A pilot showed that tokenized fund subscriptions and redemptions can be driven directly from existing ISO 20022 SWIFT messages, letting banks initiate on-chain settlement without abandoning the messaging infrastructure they already run.11 Synchronization here is between the legacy messaging network and the tokenized fund.

• The GDF / Ownera sandbox. More than seventy institutions, with thirty participating in live simulations, rehearsed using tokenized money-market funds as collateral that moves across independent networks while valuation, ownership, and compliance stay consistent. The lesson institutions drew was that tokenization will be built through interoperable ecosystems, not a single provider's ledger.

Chapter 6. The Regulatory Dimension: Compliance as Infrastructure

Compliance is where the previous two realities stop being architectural preferences and become pass/fail tests. Everything this paper has argued about privacy and fragmentation gets stress-tested the moment a regulator asks a deceptively simple question: can you prove this asset obeyed the rules - every rule, in every jurisdiction it touched, at every moment it moved, and across every ledger it lived on? A tokenized asset cannot remain compliant across fragmented chains if its compliance rules do not dynamically synchronize with its data layer; a whitelist that is current on one chain and stale on another is not a control, it is a liability. This is why regulation belongs at the center of the story rather than the end of it. It is not a separate hurdle bolted on after the technology works, but rather the discipline that determines whether the synchronization layer works at all.

There is a reason institutions are building permissioned and compliance-aware versions rather than simply using public DeFi: tokenized securities remain fully subject to securities law, and the regulatory perimeter is hardening, not loosening. In the United States, the GENIUS Act, the first federal framework for stablecoins, was signed into law in 2025, giving institutions a defined basis for the cash leg of on-chain settlement.12

Market-structure legislation (the CLARITY Act) has advanced through the House but, as of mid-2026, remains pending in the Senate, leaving the rules for tokenized securities and their infrastructure to firm up over the coming period.

The strategic implication is that compliance cannot remain a periodic, after-the-fact review bolted onto a tokenization project. It has to become part of the infrastructure. The most advanced deployments already encode investor eligibility, transfer restrictions, sanctions screening, and jurisdictional limits directly into the transaction, evaluated before execution rather than verified afterward, so that the rules travel with the asset wherever it goes.

This is where the privacy and cross-chain realities meet the regulatory one: a tokenized private credit fund moving across ledgers must carry its whitelist and its restrictions with it, enforce them at the protocol level, and do so without exposing the underlying investor data. Compliance, in other words, becomes a programmable service delivered by the synchronization layer — and for institutions operating across multiple jurisdictions, that capability may prove as valuable as the efficiency gains tokenization is usually sold on.

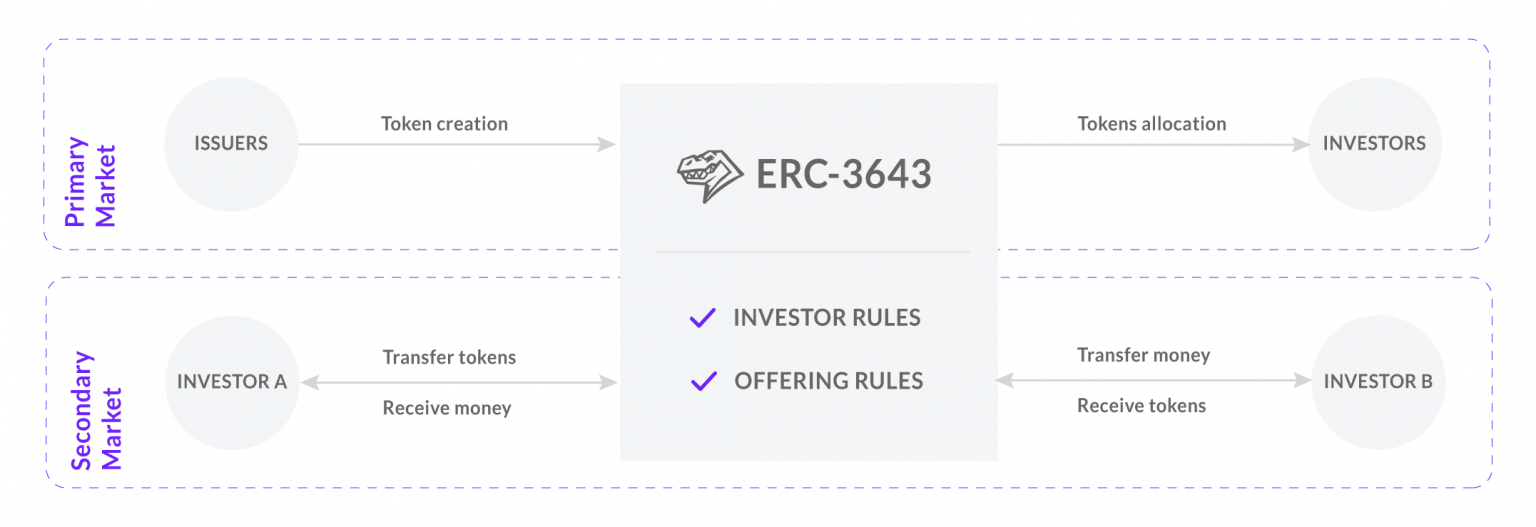

A useful illustration of this principle is the growing adoption of ERC-3643, an Ethereum token standard designed specifically for regulated financial assets. Unlike conventional token standards that simply represent ownership, ERC-3643 embeds compliance directly into the token itself through on-chain identity registries and programmable compliance modules.

Before any transfer is executed, the protocol verifies that both the sender and recipient satisfy predefined requirements, including KYC/AML status, investor eligibility, jurisdictional restrictions, and issuer-defined transfer rules. If any condition is not met, the transaction is rejected at the smart-contract level before settlement occurs.

This allows regulated securities to move across public blockchain infrastructure while ensuring that compliance travels with the asset rather than relying on manual checks after the fact. In practice, ERC-3643 demonstrates how compliance is evolving from a legal process into programmable infrastructure, providing a blueprint for how tokenized funds, private credit vehicles, and other regulated RWAs can remain compliant even as they move across multiple wallets, custodians, and blockchain networks.

Chapter 7. The Structural Orchestrator Shift

Every infrastructure transition mints a new kind of leader. Electronic trading turned exchanges into technology companies. The ETF turned manufacturing-plus-distribution into a moat. Tokenization is producing its own archetype: the Structural Orchestrator - an institution that controls multiple layers of the value chain at once, collapsing the historical separation between issuance, distribution, compliance, settlement, and the data that connects them.

The pattern is visible.

J.P. Morgan, through Kinexys, issues a deposit token and is building the payment, interoperability, and settlement rails around it.

Securitize sits across issuance, transfer agency, investor onboarding, and compliance for many of the largest tokenized funds.

Circle pairs stablecoin infrastructure with a tokenized money-market product

Stripe's acquisition of Bridge folded stablecoin payments into a broader stack.

In each case, the strategic logic is the same: the more of the lifecycle an institution controls, the fewer reconciliation seams exist between creating an asset and settling it, and synchronization infrastructure is the connective tissue that makes that integration possible.

This realigns where value accrues. Much of today's financial plumbing is paid to reconcile - to maintain separate records and repeatedly re-verify information that already exists elsewhere. Corporate-action processing alone is estimated to cost the industry around $58 billion a year, with a single event touching an average of more than 110,000 firm interactions and tens of millions of dollars to process.13 That cost is fragmentation made visible. When ownership, collateral, payment, and compliance states are synchronized across a shared environment, the reconciliation layer that justifies much of that spend begins to thin. Intermediaries do not vanish; their basis of differentiation shifts from recordkeeping to orchestration.

That $58 billion is the margin earned today by the intermediaries who perform all that manual reconciliation. Synchronization does not delete that margin; it relocates it to whoever controls the data layer that makes the reconciliation unnecessary. Which means an institution that treats data synchronization as a back-office cost to be outsourced and forgotten is doing something far more consequential than it realizes: it is quietly handing the economics of its own future to the firm that owns the plumbing. The provider that synchronizes assets is sitting in the exact position from which tomorrow's settlement, collateral, and compliance revenue will be captured. In a tokenized market, control of the synchronization layer is control of the margin pool. How an institution sources that layer, therefore, determines how much of the resulting margin it retains, and how much accrues to whoever provides the plumbing.

The most underappreciated consequence is what synchronization does to liquidity itself. Traditional markets treat liquidity as static - pledged, posted, and settled inside fixed operating windows, with capital trapped while participants wait for confirmation. When ownership, valuation, and settlement update continuously, liquidity becomes mobile. Broadridge's distributed-ledger repo platform processed roughly $7.2 trillion in May 2026 alone, averaging $362 billion a day, up more than 220% year over year — and the firm's own analysis with Finadium suggests that substituting intraday distributed-ledger repo for even ~15% of activity could cut intraday liquidity-buffer requirements by 8–17%.14 This is the second-order prize: not just faster settlement, but liquidity velocity - capital that can be deployed, recalled, and re-pledged through the day rather than parked against operational friction. And it stalls instantly if the asset is tokenized on one chain while its liquidity sits on another, which is why cross-chain synchronization (Section 4.3) is the precondition for velocity, not a separate topic.

Two further shifts follow. Compliance moves from a periodic review into a programmable service, as Section 6 describes. And data stops being a byproduct of operations and becomes the operational substrate itself: the institutions that can deliver trusted, verifiable, continuously updated information will out-execute those that cannot, on settlement, collateral, and compliance alike. That is the deeper meaning of the synchronization layer. It is not a pipe between systems. It is becoming the foundation that the systems are built on.

Chapter 8. The Landscape

As tokenization moves into production, the data layer has stopped being a single, undifferentiated category. What was once described generically as "the oracle" has matured into a set of specialized synchronization architectures, each optimized for a different part of the problem — high-frequency pricing, enterprise workflow orchestration, regulated benchmark data, direct-source verification, or modular multi-asset delivery.

That specialization is a sign of the market growing up rather than fragmenting: as institutions tokenize an ever-wider range of assets, a single fixed design is unlikely to serve a real-time treasury fund, a confidential private credit vehicle, and a cross-border collateral network equally well.

The synchronization layer has accordingly become a genuinely competitive field, and the most useful way to read it is not as a contest for the "best oracle" but as a map of which architecture is built for which job. Institutions are now choosing the operational foundation their tokenized assets will run on. Each of the leading providers below approaches that foundation from a different starting point and a different core strength.

Chainlink is the most deeply embedded institutional standard, having evolved from price feeds into a full orchestration and interoperability platform. Its runtime environment, cross-chain interoperability protocol, proof-of-reserve, NAV feeds, and digital transfer-agent standard power initiatives with DTCC, Swift, UBS, Euroclear, and others. Its core strength is enterprise workflow coordination - connecting blockchains with custodians, transfer agents, fund administrators, banks, and settlement systems, which has made it a default choice for large-scale, multi-party institutional deployments.

RedStone is built around a modular synchronization model, separating data sourcing, validation, and delivery so that a single architecture can serve a high-frequency tokenized treasury, a daily-NAV private fund, and privacy-sensitive compliance metadata alike. It supports 110-plus chains and 170-plus applications and serves as the oracle for funds including BlackRock's BUIDL, Apollo's ACRED, and VanEck's VBILL, holds a primary oracle role on the Canton Network, and has extended into credit-risk intelligence through its acquisition of Credora. Its focus is flexibility - matching the genuine diversity of institutional asset data with configurable delivery rather than a single fixed design, which positions it for the multi-asset, multi-chain reality of private markets.

Pyth is a premier market-data engine, sourcing first-party prices directly from 120-plus trading firms and exchanges across 3,000-plus feeds, and now extending into institutional data distribution. Its focus is price discovery: low-latency, high-frequency market pricing delivered with first-party provenance, which makes it especially strong for tokenized equities, ETFs, treasuries, and derivatives where continuous, accurate pricing is the central requirement.

Kaiko brings the institutional, regulated market-data model on-chain, extending established financial-data infrastructure onto blockchain networks rather than originating as a DeFi-native oracle. Its focus is licensed, auditable, benchmark-compliant pricing across tokenized equities, fixed income, commodities, FX, and digital assets, delivered through enterprise-grade data infrastructure and including deployments on the Canton Network. Its strength is data governance and benchmark administration - the regulatory-grade pricing and provenance institutions need when tokenized assets must meet the same data standards as their traditional counterparts.

Chronicle and API3 share a focus on direct-source verification, minimizing the distance between authoritative data producers and on-chain consumers to prioritize provenance and auditability. Chronicle, with roots in the original MakerDAO oracle infrastructure, is increasingly relevant to tokenized funds through its proof-of-asset framework for verifying holdings and reserves. API3 publishes data first-party through its Airnode architecture and pioneered oracle-extractable-value recapture through its OEV Network. Both are strongest where transparent, cryptographically verifiable data provenance is the priority.

While no architecture is universally superior, a liquid Treasury fund, a privacy-bound private credit vehicle, a legally-anchored real estate asset, and a cross-border collateral network impose genuinely different requirements. The decision that matters is no longer "which oracle is most credible" but "which architecture fits the asset I am actually trying to synchronize."

Chapter 9. Operational Observations

Across the case studies examined throughout this report, several consistent themes emerge that characterize institutional tokenization deployments as they move from pilot programs into production.

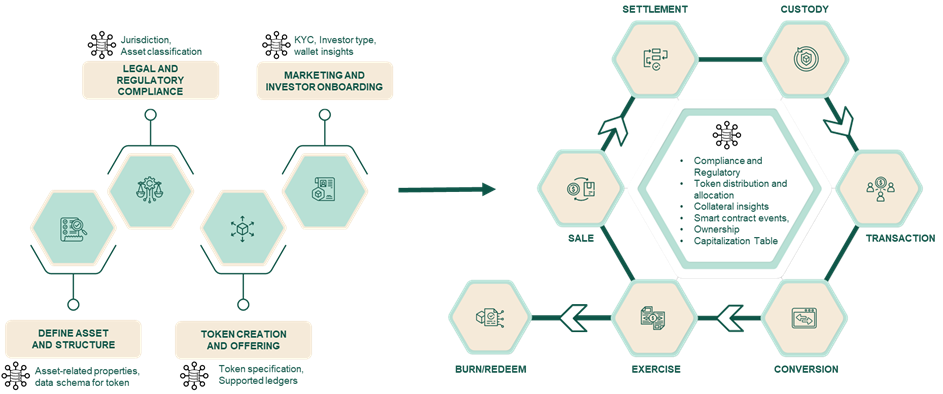

Tokenization is increasingly being designed around data lifecycles rather than digital assets alone.

Leading implementations begin by mapping valuation sources, custody relationships, compliance requirements, settlement processes, corporate actions, and reporting obligations before selecting the underlying blockchain or token standard. In production environments, the synchronization architecture is becoming as fundamental as the token itself.

Source: RedStone Report - Tokenization & RWA Standards Report

The market is steadily distinguishing production infrastructure from proof-of-concept experimentation.

While pilot programs remain valuable for testing concepts, institutional momentum is increasingly concentrated around platforms demonstrating live deployments, regulated counterparties, measurable transaction volumes, and operational resilience under real market conditions.

Interoperability has emerged as a structural requirement rather than an optional feature.

Institutions are deploying assets across public and permissioned networks simultaneously, while integrating with existing custodians, payment systems, and post-trade infrastructure. As a result, tokenization architectures are evolving toward multi-chain, multi-custodian, and cross-network models rather than isolated blockchain environments.

Compliance and independent verification are becoming embedded infrastructure services.

Rather than relying solely on periodic operational controls, production systems increasingly incorporate investor eligibility, transfer restrictions, reserve verification, proof of asset, and on-chain NAV publication directly into transaction workflows. This shifts compliance from a downstream review process toward a continuously operating component of the infrastructure itself.

Taken together, these trends suggest that institutions are evaluating synchronization infrastructure across several common dimensions: architectural flexibility across public and permissioned environments; operational efficiency at scale; security and resilience of the underlying trust layer; and the ability to support compliance, verification, and reporting as native infrastructure rather than external processes. These characteristics increasingly distinguish production-grade tokenization platforms from earlier generations of blockchain deployments.

Chapter 10. Closing Thoughts

Tokenization does not fail because assets cannot be digitized — that problem is solved. Institutions have already proven, repeatedly and at scale, that a treasury fund, a private credit vehicle, a deposit, or a collateral position can be represented on a blockchain. Tokenization fails when digital assets lose synchronization with the real-world systems that give them value. A token disconnected from its NAV, its reserves, its ownership record, and its compliance status is not a financial instrument. It is a screenshot.

This is why the framing of the entire market needs to shift. For most of the last decade, the question was can this asset be put on-chain? That question has been answered, and answering it turned out to be the easy part. The question that now decides winners and losers is a different one: can this asset stay continuously aligned with the off-chain reality it represents — accurately, cost-effectively, privately, and everywhere it trades? Everything that makes a tokenized asset useful, from collateral acceptance to lending to atomic settlement, depends on the answer. The token is the visible layer. The synchronization beneath it is where the value actually lives.

The three realities this paper has argued are not separate concerns; they are one problem seen from three angles. The economics of push versus pull determine whether the infrastructure can scale without becoming a permanent cost center. The privacy imperative determines whether the asset classes that matter most: private credit, mortgage portfolios, and the entire opaque world of alternatives, can be brought on-chain at all. And cross-chain synchronization determines whether liquidity can actually reach the asset rather than stranding it on the wrong ledger. An infrastructure that solves only one or two of these can serve crypto-native markets. Serving Wall Street requires all three at once, because the hardest institutional assets demand cost efficiency, confidentiality, and reach simultaneously.

There is also a strategic dimension that institutions underestimate at their peril. As synchronization infrastructure matures, it does not merely make existing workflows faster; it redraws the map of where value and control sit. The Structural Orchestrators — the institutions that integrate issuance, distribution, compliance, settlement, and the data layer that binds them — are positioning to capture the economics that fragmentation currently scatters across dozens of intermediaries. The firms that treat data synchronization as plumbing to be outsourced and forgotten will find, a few years from now, that they have outsourced the very layer on which liquidity, collateral mobility, and regulatory standing increasingly depend. The choice of a synchronization architecture is not a procurement decision. It is a decision about how much of the future value chain an institution intends to own.

None of this is a forecast. It is already visible in production — in a tokenized treasury fund becoming collateral across venues and then trading through decentralized liquidity, in a private credit fund becoming borrowable only once its data could be verified on-chain, in the world's largest clearinghouse rebuilding collateral management around synchronization rather than consolidation, and in central banks themselves concluding that the future of settlement is systems kept in agreement, not a single platform everyone is forced onto. The direction of travel is set. What remains contested is who builds the rails, and on whose architecture.

So the imperative for asset issuers, banks, and infrastructure providers is to start designing around the data. Map the asset's lifecycle before issuing it. Choose the infrastructure for the synchronization profile the asset actually demands. Weight production over pilots, interoperability over lock-in, and verifiable proof over issuer assurance. The institutions that internalize this will not just tokenize assets; they will operate functional, real-time markets in them. The institutions that do not will discover that they have built beautifully on top of a foundation that quietly drifts out of sync with reality.

The next phase of this market will not be defined by who issues the most tokens. It will be defined by who builds the most effective infrastructure for keeping those tokens continuously connected to valuation systems, collateral records, compliance frameworks, ownership registries, and settlement networks — privately enough for institutions to trust, and across enough ledgers to matter.

The synchronization layer is not an ancillary component of tokenization infrastructure, but rather the infrastructure itself.

Disclaimer

The organization that authored this report holds a position in RedStone, one of the tokenization infrastructure providers discussed herein. Other than RedStone, the author of this report and the author’s organization do not have any relationship that affects the objectivity, independence, and fairness of the report with other third parties involved in this report. The sources of the information and data cited in this report are considered reliable by the author, and certain verifications have been made for authenticity, accuracy, and completeness but the author makes no guarantee for the authenticity, accuracy, or completeness of the information and data cited in this report. The content of the report is for reference only, and the facts and opinions in the report do not constitute business, investment, or other related recommendations. The author does not assume any responsibility for the losses caused by the use of the contents of this report. Readers should not make business or investment decisions based on this report and must always use their independent judgment when making business and investment decisions. The information, opinions, and inferences contained in this report reflect the judgments of the researchers on the date of finalizing this report. The author undertakes no obligation to update this report following changes that might impact the opinions and inferences contained in this report. The copyright of this report is owned by Bering Waters Ventures. If you need to quote the content of this report, you must indicate the source. You may not quote, delete, or modify this report in a manner contrary to the original intent of the author.

Ocorian Blog, Global value of private assets held in funds rises 15.4% to another all-time high of $14.9 trillion, 12 February, 2026 (Link)↩︎

UK Financial Conduct Authority, Private market valuation practices (multi-firm review), 5 March 2025 (Link)↩︎

Ocorian Blog, Global value of private assets held in funds rises 15.4% to another all-time high of $14.9 trillion, 12 February, 2026 (Link)↩︎

Bank for International Settlements, Unified Ledger (Annual Economic Report 2023, 2025); Bank of England / BIS Innovation Hub, Project Meridian.↩︎

Securitize, BlackRock BUIDL — collateral acceptance reported by PR Newswire, June 2025 (Link)↩︎

Coindesk, UNI surges 25% on BlackRock investment, 11 February, 2026 (Link)↩︎

The Block, Tokenization firm Securitize taps RedStone as first oracle for onchain funds from Apollo, BlackRock and others, March 12, 2025 (Link)↩︎

Coindesk, DTCC builds out blockchain-based collateral system with Chainlink integration, March 12, 2026 (Link)↩︎

Kinexys by J.P. Morgan brings bank payment rails to tokenized asset markets with Chainlink and Ondo Finance, May 17, 2025 (Link)↩︎

State Street, State Street Investment Management and Galaxy Digital Bring Cash Management Onchain, May 05, 2026 (Link)↩︎

SWIFT, Swift, UBS Asset Management, and Chainlink successfully complete innovative pilot to bridge tokenized assets with existing payment systems, November 5, 2024 (Link)↩︎

The Whitehouse, Fact Sheet: President Donald J. Trump Signs GENIUS Act into Law, July 18, 2025 (Link)↩︎

PR Newswire, Chainlink and 24 Leading Financial Market Participants Advance Industry Initiative To Solve $58 Billion Corporate Actions Problem, September 29, 2025 (Link)↩︎

Broadridge, Broadridge’s Distributed Ledger Repo Achieves 220% Year Over Year Growth; Processes $7.2 Trillion in May, June 8, 2026 (Link)↩︎